In a world where interest rates struggle to move, investors seek safe havens for their savings. Fixed deposits and free deposits are often at the center of considerations. While fixed deposits attract with stable interest rates, free deposits offer the flexibility of a chameleon. Both options have their own advantages and challenges, which is important to understand. This article highlights the differences and provides a clear guide to make the best decision for your financial future.

The Art of Safe Investing: Fixed Deposit vs. Free Deposit in Times of Low Interest Rates

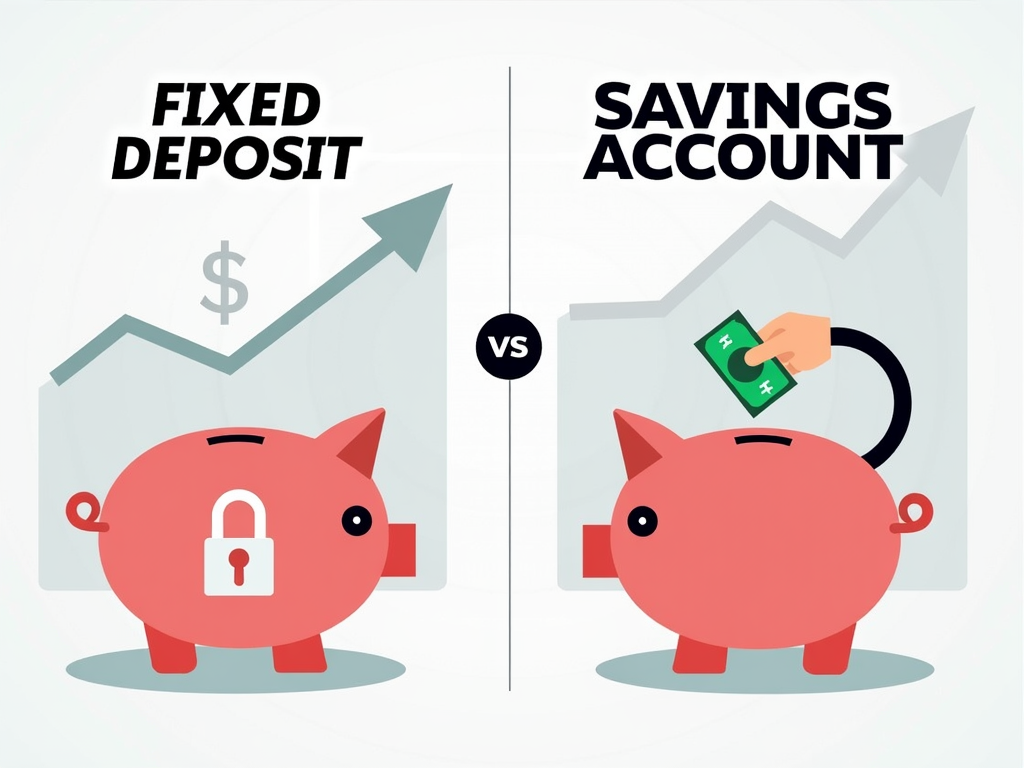

In an era of persistently low interest rates, the search for safe investment forms for hard-earned savings is crucial. Two main options that investors should consider are the fixed deposit and the free deposit. Both offer unique advantages and are suitable for different financial needs.

The free deposit stands out for its flexibility. This form of investment allows access to the invested capital at any time. It is therefore an ideal choice for short- and medium-term savings goals and for a strategic emergency reserve. Particularly convincing is the continuous security of deposits within the EU, which protects funds up to €100,000 per person and bank. However, the interest rate of this investment remains variable, which in times of declining market rates can lead to potentially lower yields.

In contrast, the fixed deposit is characterized by a fixed interest rate and a defined duration. This combination allows the investor to achieve a guaranteed return, offering a high degree of certainty in planning. Compared to free deposits, fixed deposits often offer investment options with more attractive interest rates, especially for longer maturities. However, these advantages come at the cost of lesser flexibility. During the deposit period, funds are tied up, and early withdrawal may incur significant costs. Additionally, in the case of long-term fixed accounts during periods of high inflation, there is a risk that the real return may decrease.

The choice of the most suitable form of investment should be made through a careful assessment of individual criteria: the need for flexibility and return objectives play a crucial role here. While the free deposit offers optimal adaptability, fixed deposit offers often boast higher return prospects. At the same time, risk aversion must be considered: both forms of investment are protected by deposit security; however, fixed deposits are more rigid in their liquidity. Another factor to consider is the inflation expectations, which during periods of high interest rates could reduce the attractiveness of fixed deposits.

An effective strategy in the current interest rate environment could represent a combination of both products. Intelligent wealth planning exploits the flexibility of the free deposit while enhancing return opportunities through fixed-rate offers. The staggered strategy, in which investments in fixed deposits occur with staggered maturities, is also suggested. Furthermore, it may be advantageous to examine offers from European abroad to benefit from potentially higher interest rates. The correct choice and combination of these instruments can help investors achieve their financial goals despite unfavorable market conditions.

Finding the Right Providers: Interest Rate and Security in Fixed Deposit and Free Deposit

In times of persistently low interest rates, it is essential to choose wisely to invest savings in fixed deposit or free deposit safely and profitably. The choice of the right provider plays a central role, as financial strength, deposit security, and customer service are the fundamental pillars for building trust and ensuring security.

Provider Assessment

The financial strength of a provider is an essential indicator of its financial stability. Ratings from reputable agencies such as Moody’s or Standard & Poor’s can provide useful guidance. High ratings indicate strong repayment capacity and therefore reduced risk.

Likewise, deposit security is fundamental, as it covers deposits within the EU up to €100,000 per customer and bank. This offers a guarantee of safety in case of bank insolvencies. Additionally, customer service should not be overlooked. Transparent service that reliably responds to inquiries contributes significantly to investor satisfaction.

Interest Rates

The effective interest rate provides information about the real yield of your investment, as it takes into account any ancillary costs. Therefore, it’s important to always keep an eye on the effective interest rate when comparing fixed deposit and free deposit offers. In particular, in a period of low interest rates, a rate guarantee for fixed deposit contracts can be attractive, as it protects against rate cuts. Free deposit accounts, on the other hand, offer the flexibility to benefit from rate increases, which can be advantageous in a dynamic interest market.

Security and Flexibility

The aspect of security is integrated with the issue of flexibility. Generally, fixed deposits offer higher interest rates, but at the cost of lesser flexibility, as capital is tied up for a specified period. Free deposits, on the other hand, stand out for their availability at any time, making them more attractive for unforeseen financial situations.

By carefully evaluating these criteria – financial strength, deposit security, customer service, and interest rates – investors can optimize not only the security but also the profitability of their investment during low interest rate periods. Thus, the interaction between security and flexibility becomes a strategic advantage in wealth planning.