Government bonds are the cornerstone of global financial markets, offering stability and reliable returns. But how do U.S. bonds compare to those of Japan? While the U.S. attracts with higher yields, Japanese bonds offer stability in another form. This article highlights the differences in yields and the associated currency risks, providing valuable insights for investors choosing between these two options.

Yield Dynamics of American and Japanese Government Bonds: Economic Forces and Market Expectations

The world of government bonds, particularly those from the U.S. and Japan, reflects the different dynamics of the global economic situation. The assumptions that lead to a significant discrepancy in yields between these two countries are closely tied to their underlying economic conditions and monetary policy strategies.

Economic Fundamentals and Monetary Policy

The divergent development of inflation rates and economic growth between the two nations forms the basis for the stark contrasts in the yields of their government bonds. In Japan, inflation reached 3.6% in January 2025, a moderate but notable rate in Japan’s historical context. The Japanese economy displayed a slight upward trend in the fourth quarter of 2024, with GDP growth of 0.7%. In contrast, in the U.S., declining growth forecasts raise concerns and are reflected in the yields of U.S. Treasuries. These uncertainties often lead to a downward spiral in yields as investors prefer more stable income sources.

Yields and Market Trends

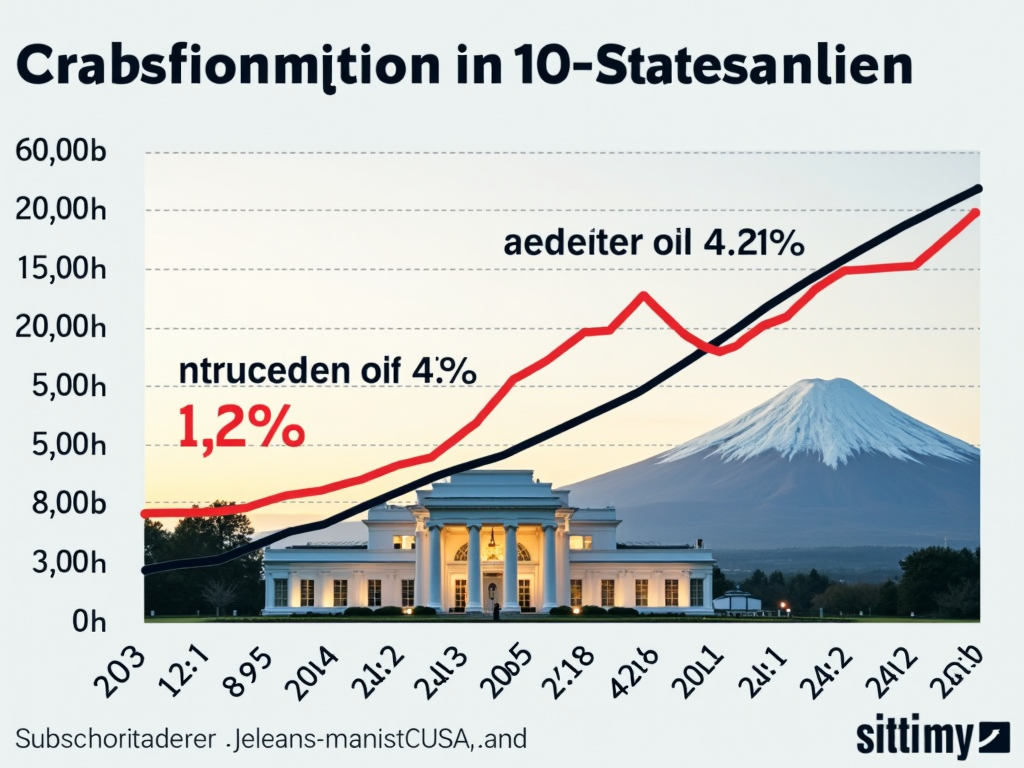

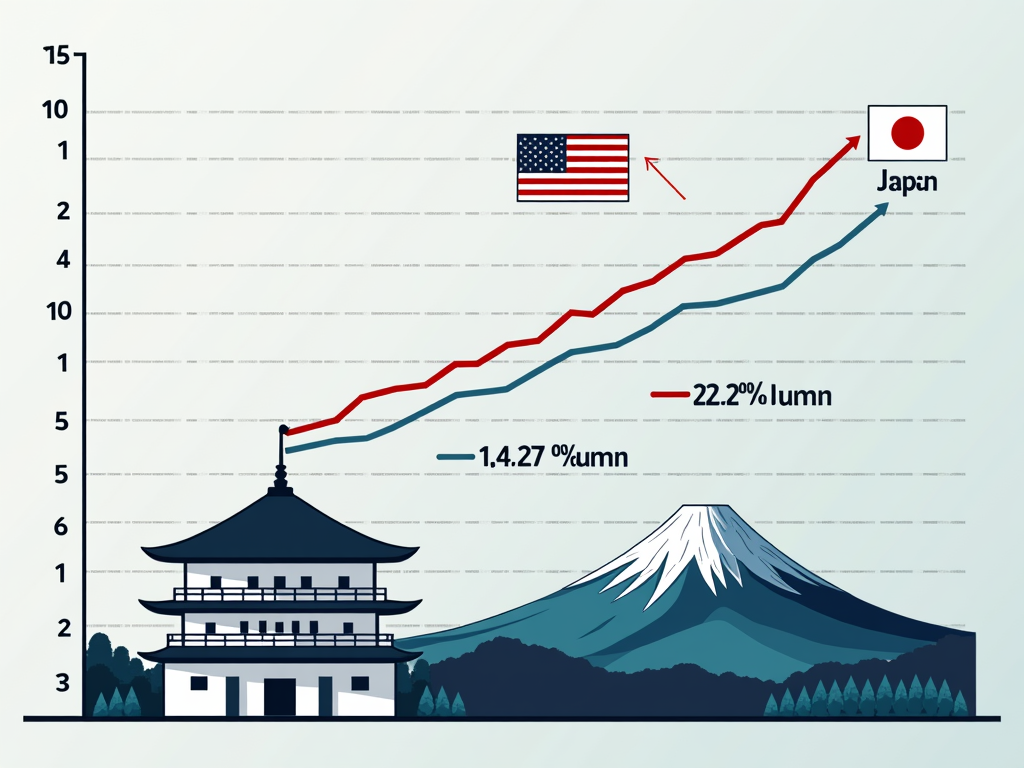

As of March 2025, U.S. ten-year Treasuries offered a yield of approximately 4.21%, while corresponding Japanese bonds yielded only 1.49%. These different levels express market expectations. In the U.S., concerns about the stability of economic policy and potential inflationary risks lead to higher yields. In Japan, on the other hand, traditionally lower yields underscore the Bank of Japan’s long-term strategy to combat deflation with an expansive monetary policy.

Competitive Pressure and Effects of Currency Policies

The international appeal of an asset class like government bonds is often directly tied to expectations regarding exchange rate movements and differences in interest rates. U.S. interest rates, which are generally higher than those in Japan, can strengthen the dollar and thus favor a preference for investments in the U.S. At the same time, the yen has stabilized due to the Bank of Japan’s monetary measures and occasional aggressive interest rate differentials. These currency movements can significantly impact the actual returns investors achieve, emphasizing the importance of a comprehensive investment strategy.

Ultimately, the yield differences of government bonds from the two nations reveal the various economic and political challenges they operate under. The decision on which of these markets to invest in depends on a range of factors, from individual investors’ risk preferences to long-term return objectives.

Currency Risks and Their Consequences on U.S. and Japanese Government Bonds

The international trade in government bonds is often associated with the risk of exchange rate fluctuations, especially when investing in large markets like the U.S. and Japan. Investors must carefully consider currency risk to avoid distorting the actual returns of their investments due to exchange rate movements.

U.S. government bonds, attractive for their high yields, carry with them, in addition to stability, a significant currency risk. This risk manifests itself through dollar volatility. In the event of a depreciation of the dollar against the investors’ domestic currency, a yield that initially appeared attractive could quickly diminish. Conversely, an appreciation of the dollar could reward the investment. An illustrative example shows that a U.S. government bond with a nominal yield of 4.3% in the case of a 3% depreciation of the dollar actually yields only 1.3%. Besides exchange rate volatility, investors must also consider interest rate risk, as any changes in U.S. interest rates can significantly affect the market value of the bonds held.

By comparison, Japanese government bonds are known for their low nominal rates, primarily due to Japan’s persistent expansive monetary policy. The yen, known for its stability, still carries a currency risk that can be further amplified by carry trades. Investors borrowing in yen to invest in higher-yielding assets could find themselves on the wrong side of currency fluctuations, which could significantly reduce their available gains upon sale. An appreciation of the yen could significantly reduce yields or even take them into negative territory.

The issue of exchange rates should not be underestimated when assessing investment returns. For investors, this means that they must minimize their currency risks through strategic measures. These include using currency derivatives to limit exposure to exchange rate fluctuations, as well as conscious portfolio diversification. Additionally, continuous market monitoring should not be overlooked to respond quickly to changes in economic conditions. Understanding and managing these currency risks will be crucial in determining whether investing in U.S. or Japanese government bonds is truly profitable in a globalized financial market.