The pension plan is an essential task that lays the foundation for a worry-free retirement. In Germany, the three-pillar model represents the basis for ensuring financial security during retirement years. While the state pension is only part of the puzzle, private pension strategies are gaining increasing importance. This article explores the structure and significance of the three-pillar model and provides insights into practical strategies for optimizing private pension products and state financing. Let’s discover together the best ways to make your retirement comfortable.

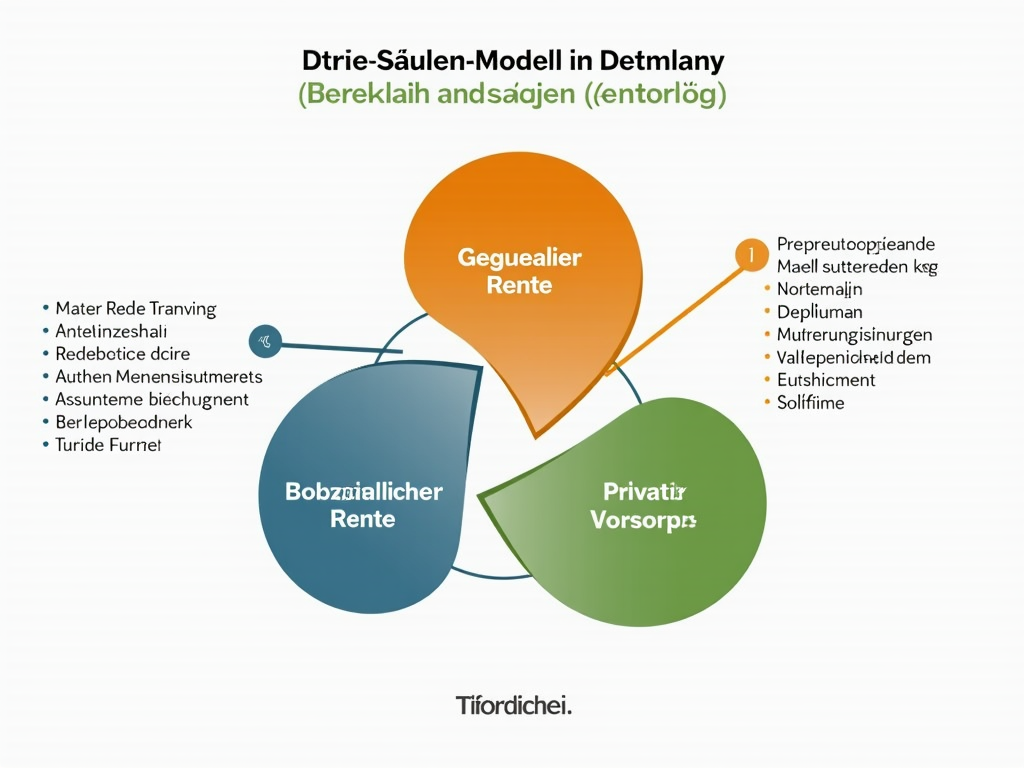

The Three-Pillar Model of the Pension Plan: Foundation of a Secure Retirement

The three-pillar model of the pension plan in Germany offers a comprehensive basis for ensuring the standard of living in retirement. It brings together statutory pension insurance, company pension schemes, and private pension savings to ensure balanced and solid pension planning. Each pillar plays a specific role and offers individual benefits that, together, constitute a solid foundation for pension security.

The first pillar, the statutory pension insurance (GRV), is the core of the pension plan and is based on a pay-as-you-go system. In this system, the contributions of current workers finance the pension payments of the current retired generation. This solidarity between generations is possible thanks to the mandatory contributions of employees and employers. The GRV offers various types of pensions to mitigate the risk of income loss in old age or in case of disability.

Additionally, the company pension scheme (bAV) serves as the second pillar. This is offered by the employer and represents an important supplement to the GRV thanks to tax incentives. In Germany, workers are entitled to a company pension scheme, which can be implemented through five different methods. These include direct insurance, pension funds, retirement funds, support funds, and pension promises. This variety allows companies to create tailored pension offers to provide greater security for employees.

The third pillar, private pension savings, includes individual measures for retirement planning. The focus is on state-supported Riester and Rürup pensions, which are made particularly attractive by tax benefits. At the same time, traditional savings and investment opportunities, such as stocks or ETFs, offer a flexible and generally profitable addition to the other two pillars. In light of the demographic challenges in Germany, the importance of this pillar is growing steadily.

Together, these three pillars form a robust system, characterized by flexibility and variety. However, the model faces challenges. In particular, demographic evolution and the financial sustainability of the GRV require long-term political reforms and further promotion of private pensions. Only through the harmonious integration of all three pillars can we ensure that financial security in old age is guaranteed and that the standard of living in retirement is maintained.

Strategic Pension Plan: Optimizing Private and State-Supported Opportunities

Ensuring the standard of living in retirement requires targeted private pension savings and smart use of state funding. An approach tailored to the individual pension gap is key to a financially secure retirement. First, it is essential to determine the difference between the expected statutory pension and the desired standard of living. This pension gap indicates how much additional capital will be needed in the long term.

Based on this analysis, a sensible combination of investment strategies can be developed. Classic pension insurances provide a security-oriented base with a guaranteed minimum interest rate, while fund-linked pension insurances offer greater yield opportunities against a corresponding risk. For more risk-oriented investors, fund savings plans represent a flexible way to participate in the capital market through regular contributions. Real estate also offers long-term security, which can be further supplemented by rental yields, although market fluctuations must also be considered.

State financing products such as the Riester pension and the Rürup pension are attractive options to benefit from subsidies and tax advantages. In particular, the Riester pension stands out for its subsidies, which are particularly beneficial for families with children, while the Rürup pension is mainly of fiscal interest to the self-employed.

In addition to individual private pension savings, company pension plans provided by employers represent an additional pillar of security, made attractive due to tax benefits and employer contributions. It is important to fully exploit the advantages offered, as such benefits not only alleviate individual savings but can also increase the overall return on pension savings in the long term.

A fundamental aspect of pension savings is also the regular review and adjustment of the chosen strategies. Life circumstances change, and financial markets also undergo fluctuations. Flexibility and the willingness to adapt to changing conditions are decisive in achieving pension goals. A conscious planning approach, which integrates the three-pillar model of statutory, company, and private pension schemes, ensures sustainable financial security in old age.