The prospect of retirement should evoke an image of relaxation and enjoyment, but for many, it is also characterized by financial worries. Often, the legal pension alone is not enough to maintain the usual standard of living. Therefore, it is important to also provide for one’s future privately. This article explores the three pillars of pension provision and shows how state benefits and private pension options can be effectively utilized to ensure a peaceful retirement.

The Foundation of Security: Understanding the Three Pillars of Pension Provision

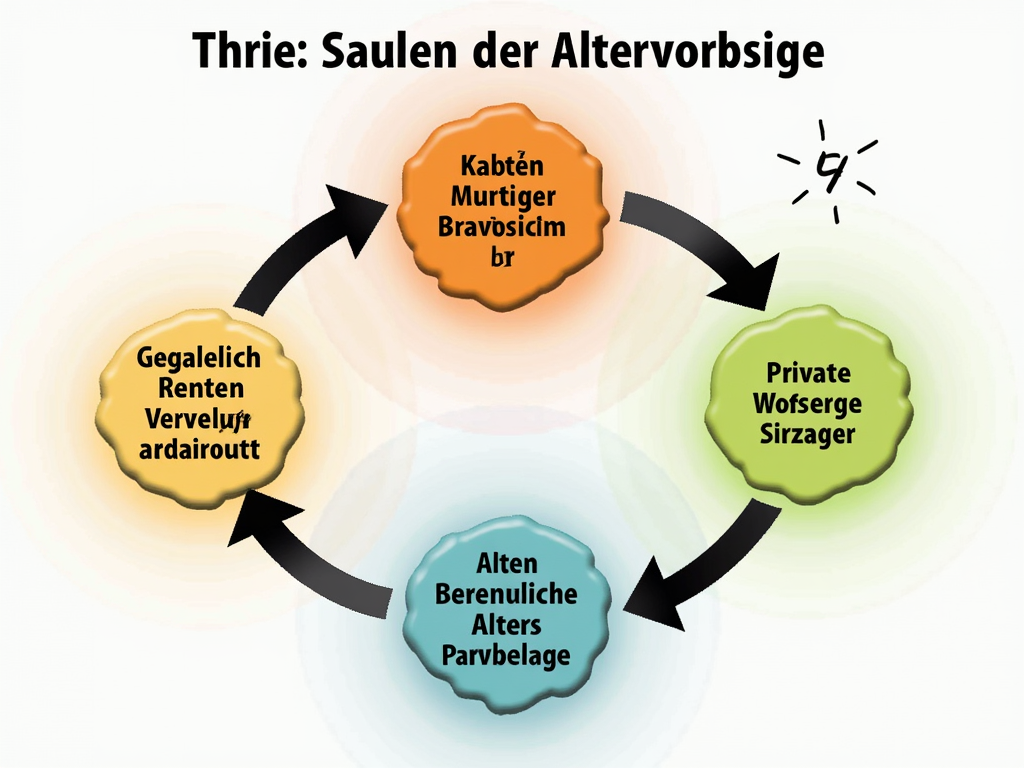

A financially secure retirement fundamentally begins with a solid understanding of the three pillars of pension provision, well established in both Germany and Switzerland. This structure allows for balanced and diversified provision that can be tailored to individual needs.

In Germany, the legal pension insurance (Pillar 1) constitutes the foundation of pension provision. It is based on a pay-as-you-go system, where the actively working population finances the pensions of current retirees. However, this alone is often insufficient to maintain the usual standard of living in old age, highlighting the need for additional pension measures.

The second pillar, corporate pension provision (bAV), represents a valuable supplement. It allows workers to generate an additional pension through their employer, often with significant tax advantages. Various implementation methods are available, such as direct insurance and pension funds, which vary depending on the employer.

The third pillar of pension provision in Germany includes private pension provision, which allows for individual supplementation to legal and corporate provision. It offers a wide range of options, from Riester or Rürup pensions to life insurance and investment models such as ETFs. The flexibility of this pillar allows for the development of customized financial strategies, which can offer tax advantages and potentially higher returns.

Structurally similar is the pension provision model in Switzerland, which is also based on three pillars. The first pillar, state old-age and survivors’ insurance (AHV), ensures that the basic needs of retirees are covered. The second pillar, professional pension provision through pension funds, protects the usual standard of living of employees. Finally, the third pillar, consisting of tax-advantaged savings plans (Column 3a) and flexible investment forms (Column 3b), completes the pension package in a personalized manner.

An effective pension provision is based on the right combination of these pillars. While legal and corporate provision serve as solid foundations, the third pillar offers the necessary leeway to meet individual preferences and financial goals. Ultimately, it is essential to start in time and make regular adjustments to optimize pension provision and ensure financial security in retirement.

With State Benefits and Private Strategies, Retirement is Secure

When it comes to financial security in retirement, state benefits and private pension options offer a compelling dual strategy. In the search for optimal coverage for future living, these options could not be more important.

The state promotes, among other things, the purchase of a home. Here, the KfW loans are particularly noteworthy, offering advantageous interest rates for constructing energy-efficient buildings or refurbishing existing properties. Home savings contracts are also supported, for example, through the “Wohn-Riester” funding, which provides up to 175 euros annually as a contribution. Furthermore, many regional programs offer additional incentives for purchasing real estate.

In the realm of pension provision, the Riester pension plays a significant role. It is particularly suitable for families and not only offers annual contributions but also advantageous incentives for children. Corporate pension provision supported by the employer further facilitates coverage in old age through tax benefits, even if it is not directly subsidized by state contributions.

Self-employed individuals or those with high incomes can benefit from the Rürup pension, also known as basic pension. This allows for the tax deduction of contributions, making it particularly attractive for the mentioned target groups. Private pension insurance represents another pillar that, despite the lack of state funding, can benefit from tax advantages in retirement.

Investment opportunities such as stocks and bond funds provide a solid basis for private pension provision. A balanced mix of ETFs and actively managed funds is advisable, as these reduce risks through diversification and increase potential returns. For more conservative investors, physical precious metals like gold can serve as wealth protection instruments.

Equally important are pension funds, which represent an interesting option for specific professional categories, such as lawyers, for additional pension coverage.

State benefits and private investments harmonize to bring the dream of secure retirement closer. It is advisable, especially in planning pension provision, to maintain flexibility and regularly review individual strategies to make the most of all available opportunities.